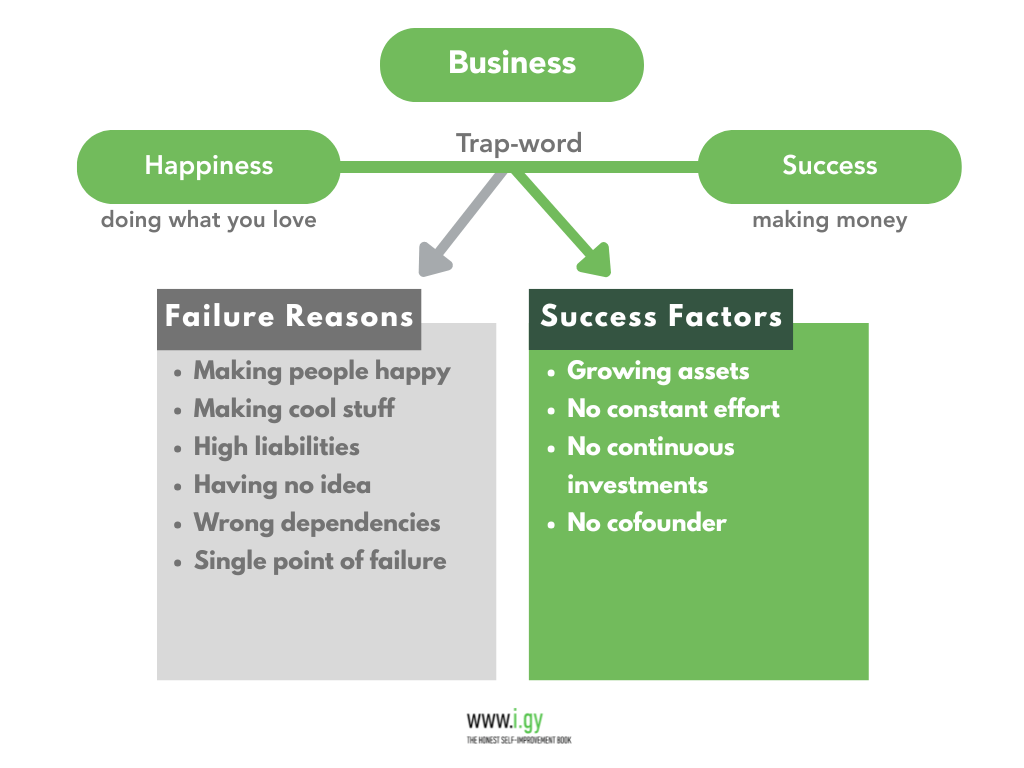

Business is more than just making Money.

Business is a Trap-word, because it’s a big complex process, and when we assign a single word to those, our brain cannot grasp the whole idea and promptly blocks further thought to prevent a confusion overload. But we’re here to clear the fog.

Imagine you have a great business idea, but you’re anxious because you don’t know exactly what you’re doing. Statistics say most businesses fail, which can be very discouraging!

How to engage your business idea, then?

Here are a few reassuring facts to get your optimism back:

- You and other people participate in a free market of goods, services, labor, attention, and information.

- Most other people don’t know shit about how to handle all this value flow and just copy everyone around them.

- Due to supply and demand laws in the free market, the more the people in the same business, the more fucked up they get.

- To give the world something with a demand that won’t be copied by many others makes you win big in the Game of Life.

- You can give it in a billion ways, the existing options are almost infinite. Try ideas wisely, following the Speed and Scaling rules.

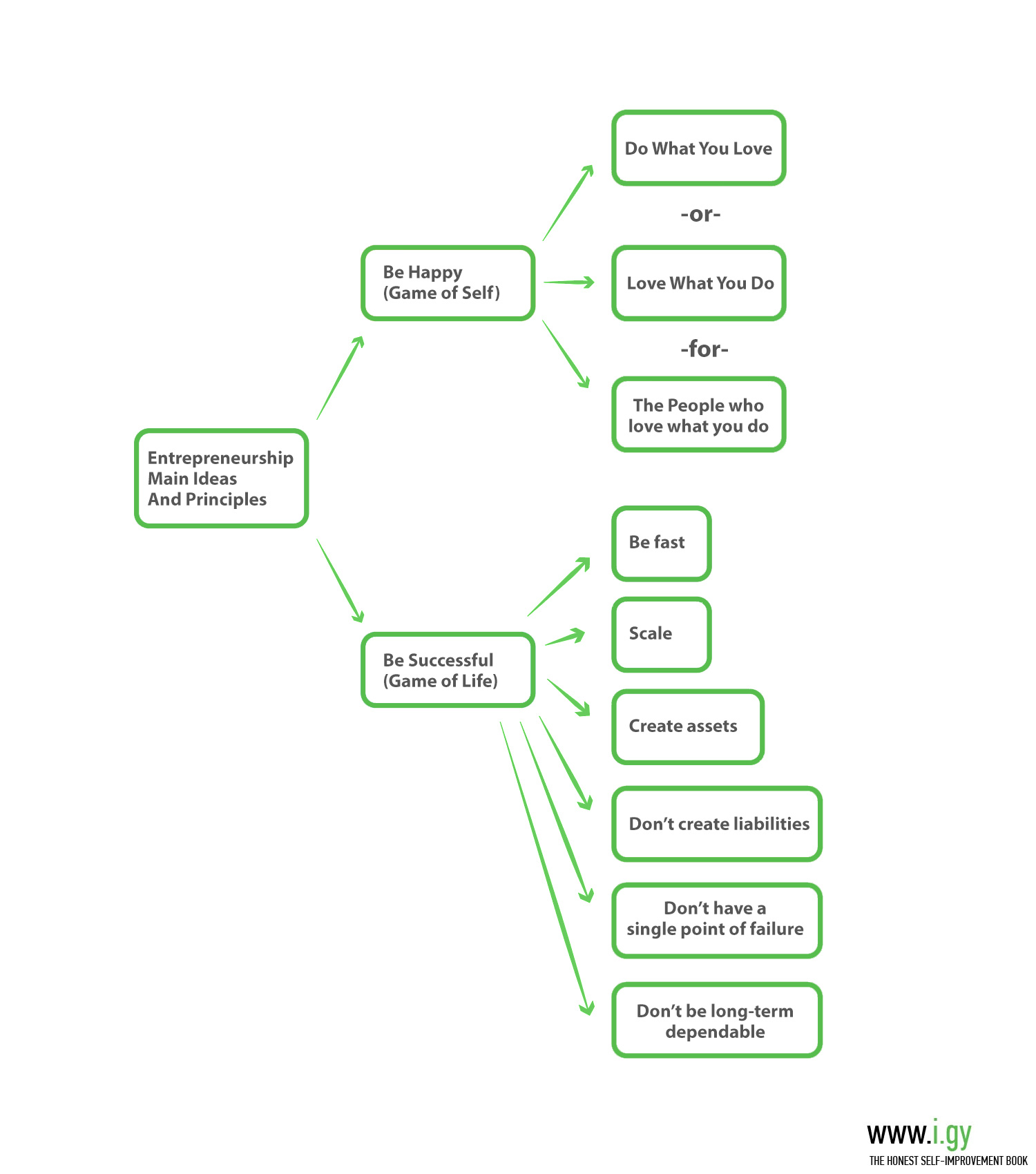

When it comes to businesses, there are two main Goals: Happiness (doing what you love) and Success (making money). Figuring out what brings you happiness is a personal journey, but let’s focus on what it means to have success. Because if you’re happy but your business goes bust, that happiness won’t last long.

Key success factors in business:

- Focus on accumulating assets over Time. If you manage to add any type of value every day/week/month, it adds up.

- Don’t trust the future. Projects that require constant investments or hard work will fail when you feel low or when times are bad. In that case, you will find yourself creating liabilities. Liabilities are the opposite of assets – they cost money, instead of generating it. These are rent, wages, bills, taxes, etc. The liability most business owners ignore is their own time and Energy they need to put into their businesses every day. If your business can’t survive without you for a week, it’s not a good business.

- Don’t have a single point of failure in a big project. Always have backup plans of similar value. There are always surprises. Don’t lean into wishful thinking.

- Don’t rely on any person, equipment, or resource that, once gone, your business cannot go without. If you have a custom-built e-commerce store, you are extremely dependent on the developers who built it for maintenance because only they know how it works. Alternatively, if you use a popular platform/CMS like Shopify or WooCommerce, you could always find new developers for maintenance who will already be familiar with the platform.

- Think about industry-level Change and how that makes your product or service obsolete. For example, the growth of e-commerce has led to the closure of many brick-and-mortar stores, impacting the retail industry big time and requiring retailers to adapt their business models.

- Don’t depend on others in the long-term. Don’t launch with an indispensable co-founder. People part ways for various reasons, and this should not end the business, too.

Side note: With the risk of sounding like your mom, I very much like “don’t…” pieces of advice. While not everyone is a fan of negative language, you have thousands of options in your life. If I suggest you do X, I limit your Freedom significantly. If I tell you don’t do X… you still have thousands of other options that actually exist and do not contain X. 99% of them are options people would define as crazy, but some of them would actually work, and the width of your idea base is precious. Tell someone what to do and you deprive them of the width. Tell them what not to do, and you not only don’t limit their Freedom that much, in the typical case of tunnel vision, you actually increase their freedom.

There are many paths to success. Don’t be afraid to explore unconventional ideas and experiment. Sometimes the craziest solutions can be the most effective!

Now let’s define the bad practices in more detail so you learn to avoid them. If you observe others engaging in bad practices and are not in a position to change their mind, at least learn from their failure – this way, you don’t have to fail on your own in every possible regard.

A really good business idea may have several points of failure and can always be resurrected into existence.

However, if there is a potentially probable event that obliterates your business idea completely, in all its forms, this means four things:

- Enormous pressure

You’ll have to live with the possibility of failure that is outside your control. This will create tons of extra pressure on you.

- Difficulty in finding employees and investors

Even if you are able to live with the risk, others may not like it. You will have a harder time finding employees, partners, and investors.

- Lower ROI

Have you ever heard of the Gambler’s Fallacy? We tend to think that just because something hasn’t crashed yet, it won’t. This is actually completely false. Make no mistake, from a probability standpoint, your project’s overall return on investment is lower if a single point of failure is present.

- Lack of flexibility

Ideas with single points of failure are not flexible in general and probably have other points of complete or partial failure you didn’t think about yet.

The moral is to have flexible ideas and, if possible, multiple revenue streams.

It often helps to imagine the worst possible reality for your business idea in a business sense (eg, not someone dying, but say losing all your current product supplies). Will this bring you down forever? If the answer is yes, try to gradually diversify until it becomes no.

A key reason why business ideas fail is the existence of the wrong kind of dependencies.

So what makes a relationship the wrong kind of dependency? I’ll give you the gold right away. It’s time again.

Short-term dependencies are perfectly fine. You must, in fact, learn to lean on employees, trust them, and delegate (which is much harder than it seems, especially if you’re a perfectionist). Time is a finite resource, and you’ll have to make compromises. It’s sometimes better for an employee to complete a task with 80% efficiency, instead of you nailing it at 98%, because you can instead focus your valuable time and energy elsewhere.

Long-term dependencies are very tricky. This usually involves your business co-founder, if you have one.

Co-founding a business with someone is like a marriage where a potential divorce would burn the business down when you aren’t able to run it individually (due to a loss of irreplaceable skill set). Proceed with extreme caution.

Your co-founder may be an amazing person, but this is just the start of the acceptance criteria.

Are you both equally and fully invested? Do your long-term visions coincide? Are there any other big projects any of you are engaged in? Does one of you still have a Day job? Or has to look after his four children and seven pets? Or looks lazy and half-motivated? Or burned out? Or just desperately wants to quit something and start anything new right now? Or drinks too much or does drugs? Or has a poor previous record of their joint ventures?

The questions are many, and any single one of these is enough for your business idea to fail. This is the price of long-term dependency.

Most people are aware of the risk of a long-term dependency (they don’t marry every person they have a crush on), yet they still often choose one to realize their idea. Why does this happen?

- You came up with the idea together (often under the influence).

- You want someone to share the responsibility with.

- You want someone to share the joy and enthusiasm with.

- You need someone to discuss your ideas with.

- You need financial support.

But when you really think about it, the first four are all about the Game of Self factors: Self-love, confidence, and obsessive morality.

Additionally, overprotection of your idea, which you likely consider your own precious child, may prevent you from sharing it openly and receiving genuine feedback. In the small bubble of anxious enthusiasm, with just you and your idea inside it, you feel compelled to welcome another “special” person so you don’t feel alone.

All of the above is rooted in a lack of Self-love and resulting insecurities, and you shouldn’t reinforce it by entering long-term dependencies.

Don’t let your initial enthusiasm cloud your perception of reality. A typical case occurs when two enthusiastic founders mutually feed each other’s hype and proceed with a business idea that is actually full of shit.

But what about money, a Game of Life factor? Sometimes the capital you need forces you to have a co-founder or investor. But even this scenario is nuanced.

If you feel you are the senior partner (more Diversity of Experience, more Resources), always consider whether you couldn’t simply hire the junior one. This can always be upgraded into a partnership later on. And you can still have fun as an employer and employee.

If you feel you are the junior partner (less Diversity of Experience, fewer resources), ask yourself whether you would have any control over the whole project at all. Never enter a partnership you have zero control over. Also, a common trap is that you expect your senior partner to contribute Time and know-how. Meanwhile, they might rather contribute only resources, and have more of an investor-like role that you don’t feel comfortable with, since this would leave the entire pressure of day-to-day operations on you.

If the co-founders are three, things get more complicated (for better or worse). While the risk of trouble increases, at least in this case, if one of the three bails out for whatever reason, the other two may be able to hold the business together. However, if there are three of you, ask yourself can the business idea survive without any single one of the founders.

Once, our (very honest) investors had to evaluate the rare case of a company with four founders. Their exact words were “a recipe for disaster”. In general, keep in mind, most long-term dependencies will fail sooner or later. Don’t expect anything to last forever. And that’s okay.

Now let’s define the most common reasons why businesses fail, so you can learn to avoid them. Even better, you won’t have to crash your business to learn something; with our fundamental principles, you’ll be able to learn from other people’s failed business ideas.

Unexpected reasons why businesses Fail

The number one reason for the failure of a business idea is… trying to make people happy!?

You try to make people happy too much while neglecting the money-earning part. Now, this can easily be misunderstood for advice to be a commercially driven asshole. This is not what I mean.

What is the most important predictor of your business idea’s success? Your Education, Diversity of Experience, and starting resources? They matter, but the world is not about you as much as you want. The number one predictor is not related to you, it’s your industry.

The entertainment industry, the food industry, and the retail industry are all focused on making people happy. And they’re all at the top of business ventures most likely to fail, along with high-liability industries such as real estate, finance, and insurance.

Let’s look at 2 real businesses – running a restaurant vs running an SEO consultancy.

______________________________________________________

Question: What is SEO?

SEO (Search Engine Optimization) is a type of digital marketing service that provides advice and resources on how to get more visitors from Google search. It’s a ~$100 billion industry.

______________________________________________________________

Running a restaurant makes people happy, creates value, and contributes to society.

Running an SEO consultancy is zero-sum in terms of creating happiness, value, and contributions to society.

You’d think that society would reward the restaurant industry more than SEO. Think again…

60% of restaurants fail within three years.1

Everyone thinks they will be the outlier to succeed, due to natural Entrepreneurship optimism and survivorship bias – a tendency to ignore failures because they’re much less visible. But you can’t argue with statistics.

In reality, it’s a tough business with endless working hours, responsibility for the clients’ health, and a number of required licenses. You cannot really pick your customers so you get a drama queen or the occasional douchebag. You need a great location, which means huge rent expenses.

Meanwhile, it’s just about impossible to fail as an SEO consultant while billing clients $100+ an hour while paying no rent, licenses, Education, or any other expenses. You do your own marketing almost for free (ranking at will in Google for “SEO + your city”), and you can easily offer the service remotely all over the world, if there is demand.

Not to mention, educating clueless people about their terrible SEO is really easy; you don’t need any long-term education. It takes only six months of full-time training to provide 80% of the value and 2-3 years to be almost perfect.

An SEO audit is usually like the service a barber gives a man who spent the last 3 years shipwrecked on a deserted island. The haircut and beard are in such a condition that any touch makes them better.

On the other hand, running a restaurant if you’ve never handled employees before or your chef only has half a year of experience will be a very-valuable-for-your-life-experience full blown disaster.

So, how is it possible that people still open restaurants, and no one outside the IT industry believes me when I tell them SEO is a gold mine?

There are two main reasons. The first one is obvious: people are not well informed about the benefits of SEO and the risks of opening a restaurant. But there’s more to it.

In the very related money post, I state that noney is the thing people believe in the most, a belief more universally accepted than Religion. But if we believe in money so much, how can we be so irrational when choosing industries?

Every restaurant founder knows even with huge effort, they will probably never get rich, but this, somehow, doesn’t stop them.

We live in a financial system (the free market) that punishes too many people who offer the same thing (supply). So, most people who want to make others happy end up stressed out in competitive, small-margin industries with a high bankruptcy rate and, ironically, sometimes unhappy themselves. It’s unfair.

Trying to make people happy gets you into overcrowded industries. So many people want to make others happy that I… actually have great hopes for the future of humanity. All this is wonderful!

If you want to make people happy, you are a wonderful human being. Just be careful about mixing this desire with business ideas and making money.

It turns out there is another strong desire that competes with financial priorities for space in people’s heads. Making people happy is the obvious one, but it doesn’t explain everything.

The number two reason why business ideas fail is… the desire to create something that doesn’t exist.

Just like wanting to make people happy, the urge to create is invaluable for humanity. We need happiness and innovation, and there is no limit, the more the better.

There is just one problem. The mathematical nature of the free market doesn’t account for these emotional human desires.

Sure, making people happy makes for great products and services. The places that have better service attract more people. Sure, creating something special leads to great products and services. The places with better food attract more people.

However, all this defines the Success of restaurants only relative to each other. Not the industry’s overall supply and overall demand.

The demand for restaurants is relatively stable. If the food is delicious, it will increase a bit, but it will reach a limit at some point.

The supply can be, well… too much. So many potential restaurant founders want to both make people happy and create something special that 60% of restaurants fail within three years, mostly due to not attracting enough customers.

Now, don’t get me wrong, I love restaurants. I couldn’t imagine my life without them, and treat everyone running or working in any of them with absolute respect. But why does a whole industry have to live on the verge of bankruptcy, creating stress for everyone working in it, often having to underpay employees or compromise on the food quality… just to survive?

All because of the 20% overly enthusiastic founders who just want to make people happy and create something special, but don’t understand economics or how they make the world harder for everyone else like them.

This is a typical example of how systems relying on rationality, like the free market, fail when colliding with the emotions of people.

And we’re talking about the best of emotions and intentions here. However, intentions are not enough – we all need much more industry understanding.

We already talked about how making stuff people like creates more restaurants than we need. Now let’s get to more extreme cases with even less desirable supply/demand ratios. In the restaurant industry, usually the primary incentive is to make people happy, and creating something different is only secondary. Reverse these priorities and you risk a total disconnection from reality.

Choosing your industry or niche just because it’s cool is not like rolling the financial dice. It’s actually worse than picking at random.

When you are driven by making people happy while getting into overcrowded industries, at least you and almost every customer have a near-perfect alignment – you want them happy, and they want themselves happy. So you’re nice, and a lot of mutual smiling takes place. You succeed most likely 90% of the Time.

Now imagine trying to create something that 90% of people would love (enough to pay for it). It’s impossible! As a result of that, not only are you in an overcrowded space, but now you have also managed to shrink the demand even more.

Take candle or jewelry making, for example. You might create a cool product and find an audience for it, but that does not create a reliable ratio.

And, consider this – thinking your product is cool does not mean it actually is.

We all tend to be very biased in this regard. So biased that we often do not want to check if our wanna-be-cool-thing already exists somewhere else. Often out of the hidden Fear that it just might, killing our amazing feeling of originality and Self-worth. If this happens, you should smack yourself back to reality and spend some good time googling and asking on related Facebook groups whether your idea does or doesn’t exist.

If creating cool stuff is not financially sustainable, you should call it a hobby, and it’s wonderful to have one. Just don’t live with the idea, the Expectations (and the resulting pressure) that it has to become a business. It may or may not, and it’s fine either way. If any pressure exists, you’re not on the right path.

Because the Game of Life has one goal above all – to get closer to reality.

Everything else is easy then. Including choosing the right Business idea that doesn’t exist. Or does. Or maybe people are on it already, like the SEO consultants. And no one believes you can earn $100+ an hour after a year of training with no previous experience. People currently stuck in Sheep mode don’t really want to explore that option.

The number three reason why businesses fail is… you create more liabilities than assets.

To evaluate a business idea, it’s very important to understand its assets and liabilities and how they project over longer periods of time. Humans are not the best at long-term valuations, so it requires experience until you start getting it intuitively.

Let’s define the two extremes.

- Assets that create money over time with no extra cost (Passive income).

We’re leaving aside cases where you own properties and rent them, since it requires a lot of starting capital. We will also avoid risky investments like the stock market. We’re trying to make Passive income possible for any middle-class person.

Passive income is massively misunderstood and used for malicious manipulation. The only case something brings you passive income is when you tested it yourself and it works long term, and it’s 100% sure it’s not a Ponzi scheme. Never believe other people, gurus, companies, courses, or ads about this.

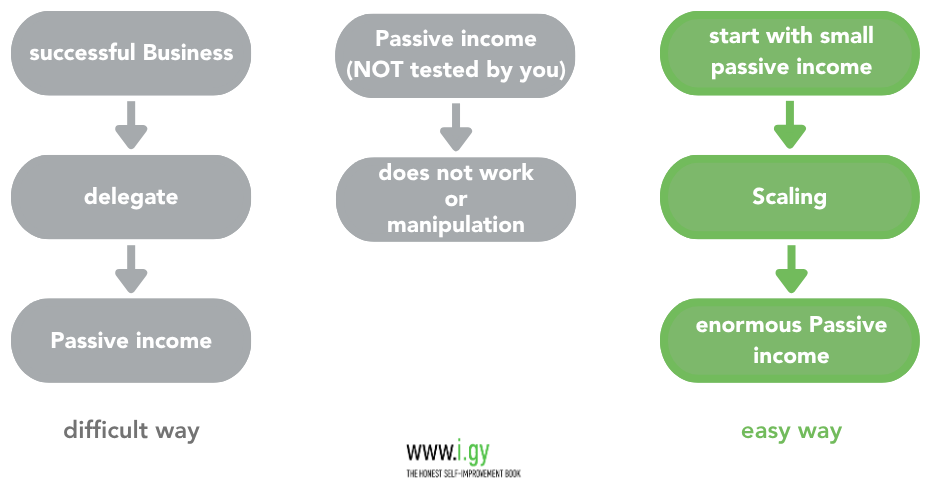

Most people’s road to passive income seems kinda backwards:

They want to have a normal income, then make it passive. This means achieving two things, one after another:

- Create a successful, sustainable business

- Delegate it to a trusted manager so you don’t have to work 24/7 for it

Both are difficult. The second part sounds easy, but considering you’ll be in maintenance mode and mostly trying to cut losses from the transition, there will be Sheep mode problems with the delegation. Also, remember that customers and partners don’t trust companies. It’s people who trust people. Whoever you put in your place to run the business needs to be trusted not only by you but by all your partners and customers. Not an easy thing.

I’ve found another path to be easier, especially in the digital world.

I’ve found another path to be easier, especially in the digital world.

Start with almost-zero-but-passive income. Say you earn $100 every month for something you do in 5 minutes a week.

Then do scaling.

Both my successful passive income streams (digital ones) happened exactly in this way. Actually, I didn’t know they were a thing before people offered me money for value I didn’t know I had. The ease was the sign I needed to do scaling. Ease is precious.

Now let’s look at the ugly extreme opposite.

- Liabilities that drain money over time with no extra benefit (burn).

Any loans fall into this category, but we’re not talking only about money here. Time is actually the most valuable asset, so any time sinks should be avoided. The most typical drains of time and energy are very annoying customers. You should try to avoid them at all costs, and being able to choose your customers is a huge business advantage.

A side note on Diversity of Experience and time:

Just learn to “feel how money stretches over time” so you can assess assets and liabilities better. It’s not natural and takes time. Sometimes, looking back helps when you get some experience. To make looking back more effective, the experience should be as diverse as possible. This often means going against usual common sense and:

- Do many things at once.

- Leave things incomplete.

Diversity of Experience is the most precious thing in the Game of Life, as it’s deep, intuitive Learning with no extra effort.

When modern Silicon Valley culture glorifies failure as a Learning experience, what they actually value is not failure; it’s the Diversity of Experience that failure always brings.

It would be weird to fail on purpose just for the Diversity of Experience. You can achieve the same result by doing many things at once and leaving non-critical things (that have exhausted their potential to give you something new) incomplete, no matter how stupid this may seem to your peers. Your journey is yours, and if you’re in it for the long run, diverse experience brings more than achievements on paper.

Finally, reason number four for the failure of a business is… having no idea, yet desperately wanting to have one.

Hello, Franchising. Not to be rude or anything, but you suck on every possible level.

Is opening a franchise ever a good idea?

It might seem like one. You feel ready to be a business owner, but don’t want to risk creating a startup. You want to invest in something reliable, so you consider joining a big traditional franchise like McDonald’s, Starbucks, Subway, or 7-Eleven.

However, opening a franchise is not a good idea if you value your freedom in business.

It’s a regrettable hybrid of having a day job and having a business, taking only the very worst from both – lack of freedom, lack of diversity, and high liabilities.

Franchising is the concept of a franchisor (usually a huge corporation) giving a business concept and resources to a franchisee (small business owner) in exchange for a cut of the sales and signing a contract where the small business signs all their freedom away, losing all their power to brand, market or differentiate itself from the main brand. This is unique from any other type of small Business – it means every time someone else fails at something, your business will suffer in association.

In my view, this is the closest you can get to actual slave labor.

It’s the worst hybrid of having a day job and having a business, taking strictly the very worst from both – lack of freedom, lack of diversity, and high risks.

Let’s just mention that franchisees are responsible for some of the worst food in the world. “Healthy, fresh food” and “Economies of scale” rarely come in the same sentence.

Basically, it’s a fucked up system which extracts maximum profit from human labor while suppressing individual creativity and the ability to grow through experience.

Also, just like slave labor, once you get in, it’s not so easy to get out. The entry barrier is often a 6-7 figure sum, most people take a loan for… so you and your employees are in for a long struggle.

Even from a purely economic perspective, the whole thing can only benefit the franchisor. Every case when you give your freedom away to a large corporation and hope that your interests have a chance against shareholder value is asking for trouble. In this sense, you take all the risks and they take most of the benefits. Initial misleading by the franchisor is so incentivized that you have to factor it in. Here is a good dive into the practices of Subway.

If you want to start a business but you have an idea that doesn’t exist yet, relax and don’t throw yourself into the first silly Direction capitalism wants to push you into. Remember, according to supply and demand rules, the best business ideas are not the mainstream ones.

You shouldn’t just sacrifice your freedom like this. Freedom is one of the basic resources in The Game of Life as it gives you the chance to take good, unexpected opportunities which life is full of once you’re in a good environment, as well as the ones that allow you to change and improve it.

We no longer live in the age where you can only try a few business ideas for your entire lifetime. The dynamics of the Internet with its instant flow of value (attention and money) in a hyper-connected system with very low costs, is a whole new world well worth exploring. You can test multiple business models within a year. Most will fail, but remember, the costs are so low and you only need to succeed once.

Most importantly, the more you try, the more you learn. In the short term (if in Hunter mode and following good practices), you can just go for it without much thought on every individual action. To quote someone who, despite his personal shortcomings, helped create better stuff than McDonald’s ever will:

Stay Hungry, Stay Foolish.

A business does not exist. Instead, think of its two components separately:

- You should be happy by making others happy or creating cool stuff (the Game of Self part)

- You should be profitable (the Game of Life part)

If you have just the first, you have a hobby, not a business, and your Expectations should be reduced accordingly.

If you have just the second, changes are needed immediately, Money can help changes, though, as noney = many kinds of Freedom. Just don’t miss out on the moment!

To be happy and sustainable, you should have them both.

But it doesn’t have to be the same activity that brings them. If you’re a Wall Street investment banker but you invest half of your money into a non-profit for building schools in Africa, and this is something that makes you happy, there is nothing missing. There is nothing bad with taking advantage of a broken system (if no people suffer as a result) if you use the resulting profits for a good cause.

By decoupling the sharing/happiness-bringing part from the money-making part, we can (maybe) rebalance the economy a bit. Otherwise, we’re doomed to repeat the cycle of the people with the best intentions ending up in the overcrowded, underpaid, and stressful industries of serving others. Just because most people are nice.

All while high-demand B2B services like SEO cost $100+ an hour from a spoiled consultant who can afford to hang the phone on any client if they simply don’t like them enough.

The key success factors in business are:

- The right industry (non-people-helping, non-cool), which you’ll spot easily if you understand the Game of Life well.

- A business model that slowly earns a lot of ioney over time and doesn’t have an ongoing burn of time/energy/money, + The ability to choose your customers.

- No single points of failure.

- Freedom, flexibility, and diverse income streams. No co-founder or a magically compatible one.

- Employees that you like and can depend on.

- The right market size- services are tough for freelancers, but not big enough to attract competition from large companies.

…. And many other mainstream things that are mentioned elsewhere. Remember, we focus on what the world ignores!

Life is unfair to many businesses, but actually, it is to your advantage. Enter industries where success exists. But don’t forget to share back with the ones left behind because of the free market, unfair information access, and human emotions. Every Taxi/Uber ride and every restaurant visit is a chance to give back to all those who don’t prioritize economics but just want to make people happy.

Life is circular.

- Parsa, H., et al. Why restaurants fail. // Cornell Hospitality Quarterly, Aug 2005.

https://www.researchgate.net/publication/237835565_Why_Restaurants_Fail

Business Ideas that Don’t Exist in Our Minds

Business – we use this word a lot,

but it sets all thinking a dot!

It is a trap that makes us block.

A new plan is there – don’t shock!

First, the right industry you choose,

so you are not going to lose.

Create cool stuff, love what you do,

but don’t forget the profit too!

Start small, but with Passive income –

that’s what makes you long-term winsome.

Second, be fast and start to scale!

Don’t let one point to make you fail!

Several streams of revenue –

you have to learn something new.

We don’t wish liability,

we need growth and mobility.

Bad customers you set apart,

no co-founder – you are smart!

You don’t have ideas? Don’t start!

When to go and wait – that’s the art!

Focus on what others ignore,

create something not done before!

‘Do this!’, ‘Do that!’ – easy to spell,

but don’ts are important to tell,

cause you’re adviced and free as well!

Now you know everything – you’re fit!

Be happy, make profit – that’s it!

Is SEO Consultancy still a good business today?

Yes, very much so.

Even for new entrants? Your business is now mature and enjoys continued success. But perhaps there isn’t room in the market for new entrants?

We actually started our own SEO agency in 2025, before this we were just in the supply chain of others. So definitely yes.